If you’re a Gen Z-er (meaning you were born between 1997 and 2012), you’re likely still in the early stages of your career, but it doesn’t mean that you should ignore financial planning. While getting professional financial advice might be the last thing on your mind, there are some things you can do to be proactive about your financial future.

We asked some monetary specialists for their best Gen Z financial advice, who came up with these five top tips for financial planning for Gen Z.

Start Saving As Early As Possible

The biggest Gen Z financial advice is to start saving as early as possible. “Gen Z should start saving for retirement as soon as possible. The sooner they start saving, the more time their money has to grow,” says Samantha Hawrylack, a personal finance expert and co-founder of How to Fire.

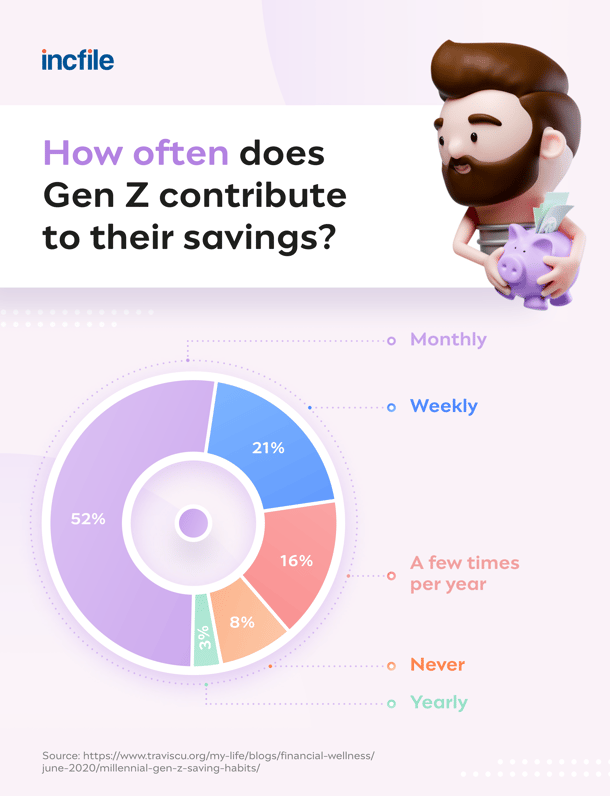

This is widely considered the biggest advantage for Gen Z-ers: Time really does equal money, and you have plenty of time on your side. One recent survey showed that 52 percent of young adults contribute to their savings on a monthly basis.

You can start small early in your career if it makes more sense to put away only a small portion. “They should try to save 10-15 percent of their income each year,” Hawrylack recommends. However, anything is better than nothing. “That’s the power of starting young: You don’t need to invest nearly as much each month because your money has plenty of time to compound, to snowball on itself,” explains Brian Davis, founder of SparkRental.

You can start small early in your career if it makes more sense to put away only a small portion. “They should try to save 10-15 percent of their income each year,” Hawrylack recommends. However, anything is better than nothing. “That’s the power of starting young: You don’t need to invest nearly as much each month because your money has plenty of time to compound, to snowball on itself,” explains Brian Davis, founder of SparkRental.

This means that with a 30- or 40-year head start, even saving a little every month and increasing the percentage slightly until the day you retire gives it a better chance to grow into a significant sum. If you don’t think about saving until the last decade of your career, it may be much harder to save a similar amount in time for your retirement.

Think About the Long-Term Goal (i.e., Retirement!)

While it might seem way too early in your life to think about retiring, Gen Z-ers who start to consider what they need in the long term can make smarter decisions in the present. In fact, a study done by The Center for Generational Kinetics found that 35 percent of Gen Z members planned to start saving for retirement in their 20s.

“This might include figuring out how much money you’ll need to live comfortably, as well as what kind of lifestyle you want to lead,” suggests Brian Meiggs, founder of My Millennial Guide. This kind of long-term vision can help you decide how much you need to save over the course of your working life to be able to retire comfortably.

Here's another way you can look at it: “Start planning the age you want to retire and work backwards,” says Shawn Plummer, CEO of The Annuity Expert. “Calculate expected monthly expenses, the guaranteed income that can be generated via retirement accounts and hence the amount you need to save.” This way you can work out a bit more of a rough figure in your head that you might try to aim for with your savings and budgeting.

Stick to a Budget and Avoid Lifestyle Creep

Budgeting is a simple but very effective financial tool, especially when used from a young age. “Young adults aren’t always looking ahead either due to lack of experience being on their own or from having lower amounts of income that make saving challenging,” explains Hawrylack. However, it’s important to start budgeting as soon as possible, no matter what, because the earlier you begin, the better spending habits you can develop over time.

Plus, starting young also means that you can increase your savings over time, especially if you exercise restraint with your spending. “You can increase your savings rate over time by locking in your current budget, rather than succumbing to lifestyle creep as you get promotions and start earning more. Resist that temptation to spend the extra money each month, at least for a few years, and put all the extra money into investments and savings,” explains Davis. Lifestyle creep is when you spend more money as you earn more money, which can lead to a paycheck-to-paycheck lifestyle even if you make a lot of money.

Only 66 percent of young adults say they’re on track to hitting their financial goals, according to a survey by Travis Credit Union, but having a budget to stick to can help with achieving your targets and reducing the chance of blowing out your budget.

Utilize Financial Apps

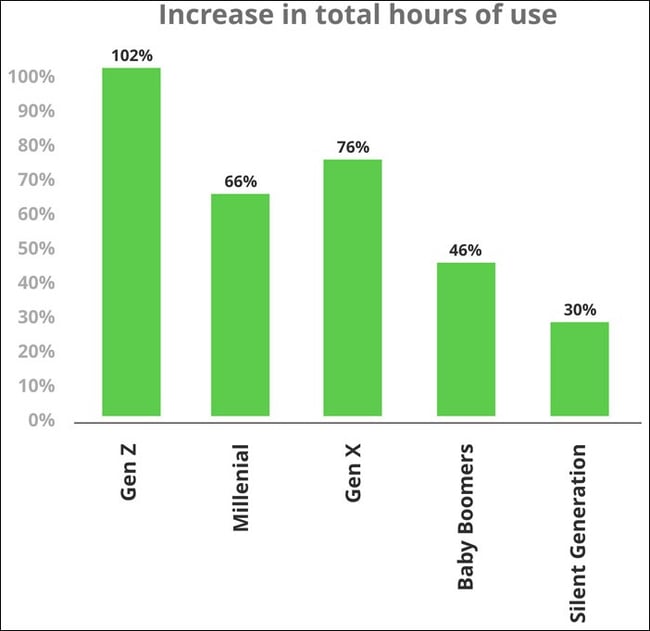

For a generation that has been brought up on social media and the internet, Gen Z is very tech-savvy and is one of the largest users of investing apps. Over the last couple of years during the pandemic, Gen Z members have increased their time spent on financial apps by 102 percent, according to an analysis done by Global Wireless Solutions.

This can be a great advantage for all aspects of financial planning with many helpful apps available. “Downloading apps such as budgeting apps also make it much easier for Gen Z to assess their expenses and start investing,” says Plummer. There are apps for everything, including tracking your spending, bookkeeping and accounting apps, planning your savings and making investments.

Brittany Kline, a personal finance expert from The Savvy Couple, recommends apps like Acorns and Digit, which are creative ways to get into saving. “With Acorns, every time you make a purchase with a linked card, the app rounds up to the nearest dollar and invests that change into a diversified investment portfolio. Similarly, Digit analyses your spending and income and looks for opportunities to save money on a daily basis,” Kline explains.

With the variety of technology available now to help with financial planning, Gen Z can develop healthy habits very early on in their working life for a more financially secure future.

Stay Informed About World Trends

Another top tip for Gen Z financial education is to stay informed about current world trends. This can have a huge impact on your financial decisions, especially if you’re looking into stocks. The world economy has a major impact on finances and cost of living, which can then impact your budget and spending habits. “For instance," says Meiggs, "if you know a recession is looming, you might want to adjust your spending habits accordingly.”

While you can’t predict everything, especially sudden events that happen down the line, if you have a general sense of the global situation, you can make more informed decisions. If you want to play it safe, then you can, as Hawrylack suggests, “Hedge your bets by investing in both inflation-proof assets and those that will benefit from rising prices.” Otherwise, self-education is key to making sure you make the right investment choices.

Plan, Stash, Save

If you want to get proactive about your financial future, the earlier you start to think about saving, budgeting and investing, the better. Gen Z is already ahead of the curve with the use of financial apps and greater access to online financial education.

There are plenty more things you can do, such as thinking about financial goals for retirement from the start and sticking to a well-informed budget. Also check out Incfile's Accounting and Bookkeeping service, which can take all of the hassle out of budgeting and taxes.

Jenna Scatena

Jenna Scatena is a writer and content strategist with a love for stories that have never been told before. More than a decade of working with prominent magazines and brands informs her approach to impactful storytelling. Her stories have reached more than 30 million readers, won multiple awards and been anthologized in books. Jenna's work has appeared in Conde Nast Traveler, Vogue, Marie Claire, The San Francisco, BBC and The Atlantic. She's the founder of the editorial consultancy, Lede Studio.